امین سیستم آرمان آمیسا

تولید و ارائه نرم افزارهای مالی و اداریامین سیستم آرمان آمیسا

تولید و ارائه نرم افزارهای مالی و اداریمفاهیم حسابداری

مفاهیم حسابداری (Accountin concepts)

مفاهیم حسابداری مجموعه قرارداد های عمومی هستند که بنای ثبت معاملات تجاری و تهیه حساب های مالی می باشد.

اهداف حسابداری (objective of accounting concept)

دارای سه هدف مهم می باشد

هدف اول: اولین هدف در مفاهیم حسابداری که هدف اصلی به شمار می رود دستیابی یا دسترسی به ثبات و نگهداری صورت های مالی می باشد.

هدف دوم: این هدف کمک به حسابداران در تهیه و نگهداری سوابق تجاری می باشد.

هدف سوم: دسترسی به درک مشترک از قوانین یا اطلاعات است که باید توسط همه نوع موجودیت ها دنبال شود که در نتیجه اطلاعات مالی جامع و قابل مقایسه را آسان می کند.

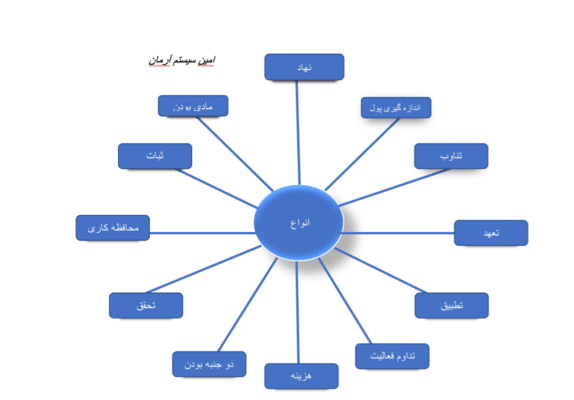

۱۲ مفهوم برتر حسابداری

توضیح ۱۲ بخش مفاهیم حسابداری:

۱:مفهوم نهاد (Entity concept)

مفهوم نهاد نشان دهنده تفاوت بین کسب و کار یک شخص میباشد. که به عنوان نهاد جداگانه شناخته میشود و بیان میکند که معاملات مربوط به تجارت باید جدا از معاملات صاحبان واحد تجاری ثبت شود.

۲:مفهوم اندازه گیری پول (money measurement concept)

این بیان می کند که فقط معاملات به صورت پولی ثبت و اندازه گیری شود.

۳:مفهوم تناوب (periodicity concept)

تناوب بیان می کند که یک سازمان یا واحد تجاری میتواند نتایج مالی خود را در دوره های زمانی معین گزارش کند.

۴:مفهوم تعهدی (Accrual concept)

بر اساس حسابداری تعهدی معامله به صورت تجاری ثبت میشود و یا به عبارتی دیگر معاملات همان طور که اتفاق میافتد ثبت میشوند.

۵:مفهوم تطبیق (matching concept)

مفهوم تطبیق بیان می کند در دوره ای که درآمد در نظر گرفته شده است واحد تجاری فقط باید هزینه های مربوط به آن دوره را در نظر بگیرد.

۶:تداوم فعالیت (going concern concept)

یک اصطلاح حسابداری برای شرکت است که از نظر مالی به اندازه کافی پایدار است و می تواند تعهدات خود را انجام دهد و به تجارت خود برای آینده قابل پیش بینی ادامه بدهد.

۷:مفهوم هزینه (cost concept)

بیان می کند که تمامی موارد به دست آمده مانند دارایی ها یا اقلام مورد نیاز برای هزینه کردن باید در بخش هزینه ثبت شود و در دفاتر نگهداری شود.

۸:مفهوم تحقق (realization concept)

این مفهوم با مفهوم هزینه مرتبط است که واحد تجاری باید دارایی را به بهای تمام شده ثبت کند.

۹:مفهوم دو جنبه (dual aspect concept)

این مفهوم بیان میکند که هر ترا کنش دارای دو جنبه بدهکار و بستانکار میباشد.

۱۰:محافظه کاری (conservatism)

مفهوم محافظه کاری بیان میکند که واحد تجاری باید دفتر حساب های خود را محتاطانه تهیه و نگهداری کند.

۱۱:ثبات (consistency)

مفهوم ثبات در حسابداری یک مفهوم است که شرکت ها باید از روش های حسابداری یکسان برای ثبت معاملات مشابه در طول زمان استفاده کنند.

۱۲:مادی بودن (materiality)

مفهوم مادی بودن نشان میدهد که صورت های مالی باید تمام موارد را نشان دهد که تاثیر اقتصادی مهمی بر تجارت دارند.

شرکت امین سیستم آرمان با ارائه نرم افزار حسابداری که با نام تجاری آمیسا قابل ارائه می باشد، توانسته نیاز بسیاری از حسابداران را برآورده کند، اکنون از این نرم افزار حسابداری در بسیاری از ارگانهای و سازمانهای بزرگ و کوچک استفاده میشود و توجه بسیاری از مدیران مجموعه ها را به خود معطوف کرده است.

![]()

Accounting concept

Accounting concepts are a set of public contracts that are used to record business transactions and prepare financial accounts.

(objective of accounting concept)

The first goal: The first and main goal is to achieve or achieve stability and maintenance of financial statements.

The second goal: This objective is to assist accountants in preparing and maintaining business records.

The third goal: is to gain access to a common understanding of the rules or information that must be followed by all types of entities, thus facilitating comprehensive and comparable financial information.

Top 12 concepts of accounting:

۱: Entity concept:

The concept of institution represents the difference between business and person.

Which is known as a separate entity and states that business-related transactions must be recorded separately from those of business unit owners.

۲: money measurement concept

This means that only transactions can be recorded and measured in monetary terms.

۳: periodicity concept

Periodicity states that an organization or business unit can report its financial results at regular intervals.

۴: Accrual concept

According to accrual accounting, a transaction is recorded commercially, or in other words, transactions are recorded as they occur.

۵: matching concept

The concept of matching states. In the period in which revenue is considered, the entity should only consider the costs associated with that period.

۶: going concern concept:

It is an accounting term for a company that is financially sound enough to be able to meet its obligations and continue its business for the foreseeable future.

۷: Cost concept

It states that all items obtained, such as assets or items required for spending, must be recorded in the expense section and kept in the offices.

۸: realization concept

This concept is related to the concept of cost that the business unit must record the asset at cost.

۹: dual aspect concept

This concept states that each transaction has two aspects, debtor and creditor.

۱۰: Conservatism

The concept of conservatism implies that a business unit should prepare and maintain its ledger on a prudent basis.

۱۱: consistency

The concept of consistency in accounting is a concept that companies must use the same accounting methods to record similar transactions over time.

۱۲: materiality

The concept of materiality suggests that financial statements should reflect all matters that have a significant economic impact on trade.

منبع: amisa.co

دوره مالی

دوره مالی (Financial period)

دوره مالی دوره ای است که عمومأ واحد های تجاری جهت گزارش های مالی سازمان یا شرکت خود از این دوره استفاده می کنند. که این دوره در بیشتر کشور ها شامل ۱۲ ماه می باشد .

ولی طبق تحقیقات سال جاری که توسط سازمان بینالمللی گزارش گری مالی انجام شده است گفته میشود. که ایالات متحده ( USA ) و کشور بریتانیا ( UK ) سال های مالی شان را ۵۳ هفته طبق اصول حساب داری پذیرفته اند.

دوره مالی یا (Financial period) به دو بخش تقسیم میشود:

۱:سال مالی (fiscal year)

۲:سال تقویم (calendar year)

سال مالی (fiscal year)

این سال مالی دوره ای است که در بخش های حسابداری دولتی مورد استفاده قرار میگیرد. و این دوره سال مالی برای هر کشور متفاوت میباشد. سال مالی مربوط به بودجه یک شرکت میباشد. که میتواند از هر قسمت سال آغاز شود.

سال تقویم(calendar year)

این تقویم سال شامل دوره ای از حسابداری میباشد که از ابتدای سال (فروردین) آغاز و آخر سال (اسفند) ختم میشود و این سال تقویم برای هر کشوری فرق دارد.

فرق بین سال مالی (Fiscal year) و سال تقویم (calendar year)

سال تقویم از اول سال آغاز و آخر سال خاتمه می یابد ولی سال مالی امکان دارد از هر قسمت سال آغاز شود به شرط اینکه ۱۲ ماه کامل شود. و یا به شرح واضح تر میتوانیم بگویم که سال مالی میتواند از وسط سال آغاز و تا وسط سال دیگر خاتمه یابد.

دوره مالی دارای ۸ مرحله میباشد :

- تراکنش یا معامله (Transaction)

- ورودی های مجله (Journal entries)

- ارسال به دفترکل (posting to general ledger)

- تراز آزمایشی (Trial balance)

- کاربرگ (Worksheet)

- تنظیم ورودی ها (Adjusting entries)

- صورت های مالی (Financial statements)

- بسته شدن (closing)

۱:معامله، تراکنش (Transaction):

تراکنش ها برای پیگیری بدهی ها، فروش ها، خرید ها و کسب دارائی ها بکار میرود.

۲: ورودی های مجله (Journal Entries):

بعد از تنظیم تراکنش مرحله بعدی ورودی های مجله میباشد که ثبت این ورودی ها در یک شرکت به ترتیب زمانی صورت میگیرد که این ورودی ها شامل: بدهکار (Debtor) و بستانکار (creditor) می شود.

۳:ارسال به دفترکل (posting to general ledger):

مرحله بعد ارسال به دفترکل میباشد و همه اطلاعات که در ورودی مجله بدست آمده است باید به دفترکل پُست شود.

۴: ترازآزمایشی (Trial Balance):

در این بخش کل موجودی حساب های یک شرکت محاسبه میشود.

۵:کاربرگ(worksheet):

خطا های که در بین حساب های بدهکار و بستانکار بوجود آمده است توسط این بخش بازیابی میشود.

۶:تنظیم ورودی ها (Adjusting Entries)

این بخش برای راهنمایی اصلاح ورودی ها ،درآمدها و هزینه های تأخیر افتاده استفاده میشود.

۷:صورت های مالی (Financial statements):

توسط این بخش سود، زیان و جریان نقدی یک شرکت را میتوان بررسی کرد .

۸:بسته شدن (closing)

این بخش شامل انتقال اطلاعات از حساب های موقت در صورت سود و زیان به حساب های دائمی در ترازنامه است که در پایان دوره حسابداری ثبت میشود.

![]()

Financial period

The Financial period is the period that business units generally use for the financial statements of their organization or company.

This period includes 12 months in most countries.

But according to this year’s research conducted by the International Financial Reporting Organization. That the United States (USA) and the United Kingdom (UK) have accepted their fiscal years 53 weeks according to accounting principles.

Financial period is divided into two parts:

۱: fiscal year

۲: calendar year

۱: Fiscal year:

This is the fiscal year used in government accounting. And this period of the fiscal year is different for each country. The financial year is related to the budget of a company. Which can start from any part of the year.

۲: Calendar year:

This calendar includes an Financial period that begins at the beginning of the year (April) and ends at the end of the year (March).

And this year of calendar is different for each country.

Difference between (fiscal year) and (calendar year):

The calendar year begins at the beginning of the year and ends at the end of the year, but the fiscal year may begin at any time of the year as long as 12 months are completed. Or to be more precise, the fiscal year can start in the middle of the year and end in the middle of another year.

Periodic accounting has 8 stages:

۱: transaction

۲: journal entries

۳: posting to general ledger

۴: trial balance

۵: worksheet

۶: Adjusting entries

۷: Financial statement

۸: closing

۱: Transaction

Transactions are used to track debts, sales, purchases and acquisitions of assets.

۲: Journal entries

After setting the transaction, the next step is the journal entries, which are registered at certain time in a company, respectively, when these entries include: ( debtor )and ( creditor ).

۳: posting to the general ledger

The next step is to send it to the general office and all the information in the journal entry should be posted to the general office.

۴: Trial balance

In this section, the total balance of a company’s accounts is calculated.

۵: Worksheet

Errors between debtor and creditor accounts are recovered by this section.

۶: Adjusting entries

This section is used to guide the correction of overdue inputs, revenues and expenses.

۷: Financial Statements

With this section, the profit, loss and cash flow of a company can be examined.

۸: Closing

This section includes the transfer of information from temporary accounts in the event of a profit or loss to permanent accounts on the balance sheet, which is recorded at the end of the accounting period.

منبع: amisa.co

حسابداری قانونی

حسابداری قانونی (Forensic accounting)

حسابداری قانونی برای بررسی تقلب در سوابق مالی یک واحد تجاری و یا یک شخص میباشد که نتایج تحقیقات حسابداری قانونی برای اثبات چگونگی جرم مالی در دادگاه استفاده می شود.

حسابداری قانونی شامل ۱۲ بخش میباشد :

- سرقت مالی (مشتریان، کارمندان و یا افراد خارجی) (Financial thefts: customers, employees or outsiders)

- تقلب در اوراق بهادار(securities fraud )

- ورشکستگی(bankruptcy )

- عدم پرداخت بدهی(defaulting on debit)

- خسارت اقتصادی(انواع دعا وی برای جبران خسارت):(Economic damage ,various type of lawsuits to recover damage )

- دعا وی مربوط به (M&A related lawsuits): (M&A)

- فرار مالیاتی یا تقلب (Tax evasion on fraud)

- اختلافات ارزش مالی شرکت (corporate valuation disputes)

- ادعای سهل انگاری حرفه ای(Professional negligence claims )

- پول شویی(money laundering )

- اطلاعات حریم خصوصی(privacy information )

- مراحل طلاق(divorce proceedings)

۱:سرقت مالی (مشتریان، کارمندان و یا افراد خارجی)

( Financial theft ( customers, employees, or outside

سرقت مالی در حسابداری قانونی برای دریافت سارق های مالی یک سازمان یا واحد تجاری که شامل کارمندان ، مشتریان و افراد خارجی است میباشد.

۲:تقلب در اوراق بهادار (securities fraud)

بعضی افراد با توجه به موقعیت فعلی خود از اطلاعات نهایی اوراق بهادار سوء استفاده می کنند که این باعث بی اعتمادی افراد به بازار سرمایه می شود.

۳:ورشکستگی (bankruptcy )

ورشکستگی وضعیت حقوقی یک نهاد انسانی یا غیر انسانی یک شرکت یا سازمان دولتی است که قادر به باز پرداخت بدهی های به تاخیر افتاده خود نمیباشد.

۴:عدم پرداخت بدهی (defaulting on debit)

این هم شبیه ورشکستگی میباشد که یک شرکت یا واحد تجاری نمیتواند آن را پرداخت کنند.

۵:خسارت اقتصادی (انواع دعا وی برای جبران خسارت):(Economic damage ,various type of lawsuits to recover damage)

خسارت اقتصادی به جبران خسارت پولی گفته میشود که در صورت عدم درآمد گذشته و آینده بوجود می آید.

۶:دعا وی مربوط به (M&A) :(M&A related lawsuits)

در این بخش روش دعا وی قضایی (M&A) مربوط به یکجا شدن مالکیت دو یا چند شرکت میشود.

۷:فرار مالیاتی یا تقلب (Tax evasion on fraud)

فرار مالیاتی بسیار مهم است که یک شخص میتواند اعلام عدم درآمد و دارایی را توسط جعل اطلاعات برای جلوگیری از پرداخت بیشتر مالیات ایجاد میکند.

۸:اختلافات ارزش مالی شرکت (corporate valuation disputes)

این اختلاف میتواند شامل اشتباهات صورت حساب مالی یک شرکت باشد که این اشتباهات باعث اختلافات ارزش مالی می شود.

۹:ادعای سهل انگاری حرفه ای (Professional negligence claims )

گاهی اوقات ممکن است شما توصیه سهل انگارانه از یک متخصص دریافت کنید که در نهایت میتواند تاثیر مالی به کسب و کارتان داشته باشد.

۱۰:پول شویی (money laundering)

پول شویی روند غیر قانونی بدست آوردن مبالغ زیادی پول است که توسط فعالیت محرمانه مانند قاچاق مواد مخدر و قاچاق انسان بدست می آید.

۱۱:اطلاعات حریم خصوصی (privacy information)

شامل اطلاعات خصوصی یک شرکت و یا واحد تجاری میباشد.

۱۲: مراحل طلاق (divorce proceedings)

در این بخش استفاده حسابداری قانونی میتواند به افشا اطلاعات ضروری در مرحله آماده سازی طلاق کمک کند.

خدمات حسابداری قانونی به ۴ بخش تقسیم میشود:

- خدمات تحقیقات جنایی (Criminal investigation service)

- خدمات حل اختلاف (Dispute resolution service)

- خدمات بررسی ادعای بیمه (Insurance claim review service)

- خدمات بررسی کلاه برداری (Fraud investigation service)

۱٫ تحقیقات جنایی (Criminal investigation service)این بخش یکی از بخش های خدماتی جنایی در حسابداری قانونی میباشد که شبیه FBI عمل میکند و همچنان در حسابداری بخشی که تحقیقات جنایی را انجام میدهد حسابداری قانونی است.

۲٫ خدمات حل اختلاف (Dispute resolution service)

در این مورد تعامل با حسابداری قانونی ممکن است ضروری باشد و برای کشف برخی موارد مرتبط با تسویه حساب عمدتا به مهارت حسابداری نیاز است.

۳٫ خدمات بررسی ادعای بیمه (Insurance claim review service)

بیشتر مواقع از خدمات ادعای بیمه که شامل سوابق مالی و حسابداری می باشد استفاده می شود.

۴٫ خدمات بررسی کلاه برداری (Fraud investigation service)

این خدمات برای دریافت تقلب کاران از سطح کارمندان تا سطح مدیریت و از پول نقد تا دارایی های با ارزش بالا آغاز میشود قابل استفاده است.

آیا میدانید نرم افزار حسابداری مناسب کسب و کار شما باید چه ویژگی هایی داشته باشد، فقط کافیست اینجا کلیک کنید.

Forensic accounting

Forensic accounting is the investigation of fraud in the financial records of a business entity or an individual. The results of forensic accounting research are used to prove how a financial offense is in court.

Forensic accounting is divided into 12 types :

- Financial thefts(customers, employees, or outsiders)

- (securities fraud )

- (bankruptcy )

- (defaulting on debit)

- Economic damage(various types of lawsuits to recover damage)

- (M&A related lawsuits )

- (Tax evasion on fraud)

- (corporate valuation disputes)

- (Professional negligence claims )

- (money laundering )

- (privacy information )

- (divorce proceedings )

۱: Financial thefts (customers, employees, or outsiders)

Financial theft in statutory accounting is to receive obtain theft from an organization or business unit that includes employees, customers, and outsiders.

۲: Securities fraud

Some people misuse final information due to their current situation, which destroys people’s trust in the capital market.

۳: Bankruptcy

Bankruptcy The legal status of a human or non-human entity is a government company or organization that is unable to repay its arrears.

۴: defaulting on debt

This is similar to bankruptcy that a company or business unit cannot pay.

۵: Economic damages (various types of lawsuits to recover damages)

Economic loss is the compensation for monetary damage that occurs in the absence of past and future income.

۶: M&A related lawsuits

In this section, the litigation method (M&A) is related to the joint ownership of two or more companies.

۷: Tax evasion on fraud

Tax evasion is so important that a person can create a declaration of non-income and assets by falsifying information to avoid paying more taxes.

۸:corporate valuation disputes

This discrepancy can include errors in a company’s financial statements, which can lead to discrepancies in financial value.

۹:professional negligence claims

Sometimes you may receive negligent advice from an expert that could ultimately have a financial impact on your business.

۱۰: Money laundering

Money laundering is the illegal process of obtaining large sums of money obtained through covert activities such as drug trafficking and human trafficking.

۱۱: Privacy information

Contains private information of a company or business unit.

۱۲: divorce proceeding

In this section, the use of legal accounting can help to disclose the necessary information in the divorce preparation phase.

The service of forensic accounting is divided into 4 types

- (Criminal investigation service)

- (Dispute resolution service)

- (Insurance claim review service)

- (Fraud investigation service)

۱: Criminal Investigation Services

This is one of the criminal services departments in forensic accounting that acts as the FBI and is also in the accounting department that conducts criminal investigations.

۲: Dispute resolution services

In this case, interaction with statutory accounting may be necessary and accounting skills are mainly required to discover some items related to the settlement.

۳:Insurance claim review services

Insurance claims services, which include financial and accounting records, are often used

۴: Fraud investigation services

These services can be used to find fraudsters from the employee level to the management level and from cash to high-value assets.

منبع: amisa.co

گزارش عملکرد مالی

گزارش عملکرد مالی (The financial performance reporting) یکی از مهمترین وظایف عمده حساب داری به شمار میرود و هدف گزارش این عملکرد مالی متعهد کردن واحد های تجاری و بیان اطلاعات مالی یک شرکت می باشد.

گزارش عملکرد مالی شامل این ۴ بخش میباشد:

- ترازنامه (Balance sheet )

- صورت جریان نقدی (Cash flow statement )

- صورت حساب درآمد (Income statement)

- صورت های مالی (Financial statement)

۱:ترازنامه (Balance sheet)

شامل حساب های مالی یک شرکت میباشد که این حساب های مالی شامل:

- بدهی (debits)

- کل بدهی ها (Total debits)

- دارائی ها (Assets)

- سرمایه صاحبان سهام (Equity of shareholders)

۲:صورت جریان نقدی (cash flow statement)

یک صورت مالی است که همه اطلاعات را در مورد جریان های نقدی یک شرکت که جهت خدمات خود دریافت میکند ارائه میدهد و همچنان برای سرمایه گذاری در یک دوره معین پرداخت میشود.

۳:صورت حساب درآمد (Income statement)

یک گزارش عملکرد مالی که نشان میدهد چگونه درآمد را به درآمد را خالص (net income) یا سود خالص (net profit) تبدیل کرد و همچنان هزینه های شرکت را در یک دور معین نشان میدهد و یا میتوان گفت که سود و زیان یک شرکت را نشان میدهد

۴:صورت های مالی (Financial statement)

صورت های مالی جهت دانستن سوابق رسمی فعالیت های یک شرکت و همچنان نشان دهنده وضیعت مالی یک شرکت جهت سود وزیان آن می باشد

The financial performance reporting

Its one of the important accounting tasks and the purpose of this financial performance report is to commit business unit and express a company’s.

Financial performance reporting is divided into 4 types

۱: balance sheet (BS)

۲: cash flow statement (CFS)

۳: income statement (IS)

۴: financial statement (FS)

۱: balance sheet:---

the balance sheet includes the financial account of a company that theses financial accounts include :

- ۱: debits

۲: total debits

۳: assets

۴: equity of shareholder

۲: cash flow statement:

is a financial statement that provides all the information about the cash flow of a company that receives for it service and is still paid for the investment in a certain period.

۳: income statement:

is a financial statement that shows how an income is converted into net income or net profit and also shows the expenses of a company in a certain period or shows the profit and loss of a business unit.

۴: financial statement:

is to know the official records of a company’s activity and also show the financial situation of a company for its profit and loss.

منبع: amisa.co

حسابداری مدیریتی

Management accounting system سیستم حسابداری مدیریتی

در حسابداری مدیریتی باید همه اطلاعات مالی و غیر مالی به مدیران ارائه گردد و مدیران با استفاده از اطلاعات اخذ شده از طریق کارمندان برای تصمیم گیری در مورد مسایل سازمان شان وظایف کنترلی را انجام دهند.

Main point:نکته مهم

حسابداری مدیریتی با حساب داری مالی خیلی فرق دارد چون هدف حسابداری مدیریتی کمک به کارمندان داخل سازمان است.

حسابداری مدیریتی (Management accounting) به چهار بحش عمده تقسیم شده اند:

۱:cost accounting system (سیستم حسابداری بهای تمام شده)

هدف این حسابداری گرفتن کل هزینه تولید یک کسب و کار با هزینه های قابل تغییر مانند هزینه تولید و هزینه ثابت مانند هزینه اجاره می باشد که توسط این بخش انجام میشود.

۲:Inventory management system (سیستم مدیریت موجودی)

هدف این سیستم شامل مراحل:

- سفارش (order)

- ذخیره (store)

- فروش موجودی (Inventory sales) می باشد که همچنان شامل نظارت کالا های شرکت از خرید تا تولید و تا پایان فروش می باشد.

۳:Job cost accounting system (سیستم حسابداری بها تمام شده مشاغل)

هدف ار این سیستم بررسی هزینه پروژه شغل یک فرد می باشد و یا شامل هزینه و درآمد بر اساس شغل می باشد

که این هزینه به ۳ بخش خاص تقسیم می شود.

- نیروکار (work force)

- سربار (overhead)

- مواد (materials)

۴:Performance reports system(سیستم گزارش عملکرد)

این یک فعالیت مهم در مدیریت حسابداری می باشد و این گزارش عملکرد یک سند است که شرکت برای تعریف موقیعت کلی خود ایجاد میکند.

Management accounting

In management accounting all financial information and non -financial information must be provide to managers and managers must perform control tasks by using information obtained through employees to make decisions about their organization issues.

Main point: financial accounting is very different from management accounting. because the purpose of management accounting is to help employee within the organization.

Management accounting is divided into 4 types:

۱٫ Cost accounting system (CAS)

۲٫ Inventory management system (IMS)

۳٫ Job cost accounting system (JCAS)

۴. Performance report system (PRS)

۱: Cost accounting system

the purpose of this system

Is getting the total production costs of a business with variable costs (cost of production) and fixed costs

wich is done by this section.

۲: Inventory management system

the purpose of this system is to order, store and inventory sales of a company wich is also include monitoring the company’s good from purchase to production and until the end of sales.

۳: Job cost accounting system

the purpose of this system is to review a person’s job project or include expenses and income based on job.

This cost divided into 3 special types;

۱: work force

۲: over head

۳: materials

۴: performance

۴: performance report system

This is an important activity in management accounting and this performance report is a document that the company creates to define it’s over all position.

منبع: amisa.co